India’s trade deficit rose to a record high in November, led by a sharp rise in gold imports, even as exports shrank.

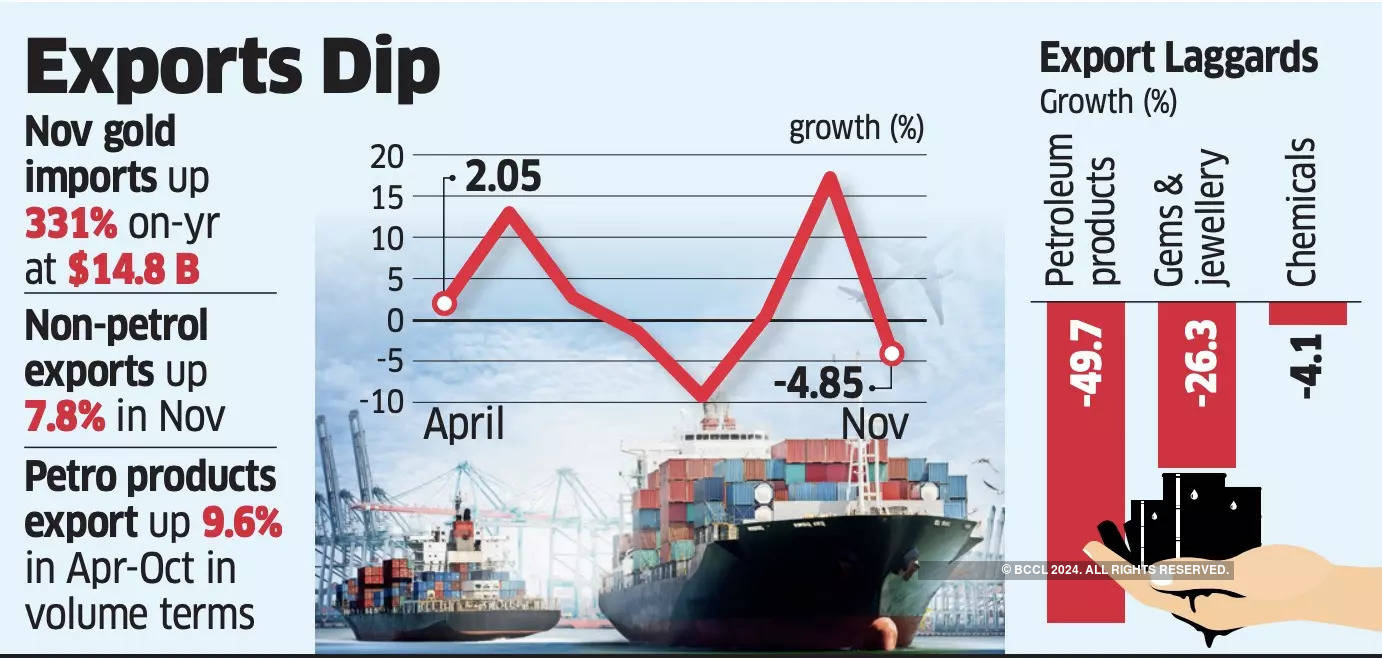

Official data released Monday showed the trade gap widened to $37.8 billion in November, up from $27.1 billion in October and $21.31 billion a year ago. Goods imports rose 331% year-on-year in November.

Merchandise exports shrank 4.9% year-on-year to a two-year low of $32.1 billion, while imports rose 27% year-on-year to a record $69.95 billion.

“An unprecedented fall in the prices of petroleum products has pushed down merchandise exports in November,” Commerce Secretary Sunil Barthwal said, adding that petroleum prices affected export growth. But he remained optimistic about export prospects.

“We are very confident that exports of non-petroleum products and services will remain steady in the next three to four months. We will cross $800 billion by a huge margin,” he said. “As long as exports and foreign direct investment (FDI) grow, that will finance our imports.” Exports of non-petroleum products increased by 7.8%. In November, gold worth $14.8 billion was imported.

Officials attributed this to demand for parties and weddings, diversification of assets towards gold amid global uncertainties, increasing demand from banks and reduction in customs duty from 15% to 6%. “Every time there is geopolitical uncertainty, we see a rise in gold imports,” Barthwal said. Non-petroleum exports rose 7.8% to $28.4 billion, compared to $26.4 billion a year ago. Overall, trade continued to grow, driven by services exports, which rose 26.9% to $35.7 billion in November, preliminary figures from the Ministry of Trade and Industry showed. “The demand during Christmas was for non-petroleum products. The demand for Indian products is growing. There was a lot of inventory build-up in October,” Barthwal said about the 17.25% increase in goods exports in October.

Federation of Indian Export Organizations (FIEO) President Ashwani Kumar said such dip in exports was mainly due to the ongoing global economic uncertainties.

“The increasing tensions between Israel and Iran have continuously led to logistical challenges regarding international trade, as most of our trade to Europe, Africa, the CIS and the Gulf region takes place via the Red Sea Route or the Gulf region, which prompts buyers to have large inventories,” he said.

In the April-November period, exports rose 2.17% year-on-year to $284.31 billion and imports rose 8.35% to $486.73 billion. Barthwal said the government is focusing on 20 countries where export potential is high, six manufacturing sectors where India has good manufacturing capacity and six service sectors including IT-ITeS. A withdrawal of commercial missions from these 20 focus countries is being planned to discuss ways to increase exports to them, he said.